What's Next for Private Equity in Healthcare?

What's Next for Private Equity in Healthcare?

It might get messy

On April 3, Senator Ed Markey (D-Mass.) released a draft bill called the “Health Over Wealth Act.” It aims to increase transparency around private equity’s involvement in healthcare, including hospitals, physician groups, and dialysis groups. Some of Markey’s proposals:

PE firms would need a license from the Dept. of Health & Human Services (HHS) to invest in healthcare

HHS could prohibit any PE healthcare deal, including from “licensed” investors

PE firms would need to report more financial & operational data, including info about debt, wages, political spending, and use of patient care facilities (hallways, waiting rooms, etc)

Markey’s bill is part of a growing effort by US politicians to control healthcare consolidation.

In this article, we’ll look at the growth of healthcare private equity, the state of recent deals, and the government’s future role in PE regulation.

Private Equity: A Scourge on Healthcare? Or a Lifeline?

The Why:

Definitive gives three great reasons for why PE is targeting healthcare:

Healthcare is recession-resistant (people will always get sick)

Waste is endemic in healthcare businesses (enabling PE firms to make them more efficient)

Providers are often geographically fragmented (so PE firms can consolidate market power + get economies of scale)

So it’s no wonder that PE involvement has increased—a lot.

Current Data:

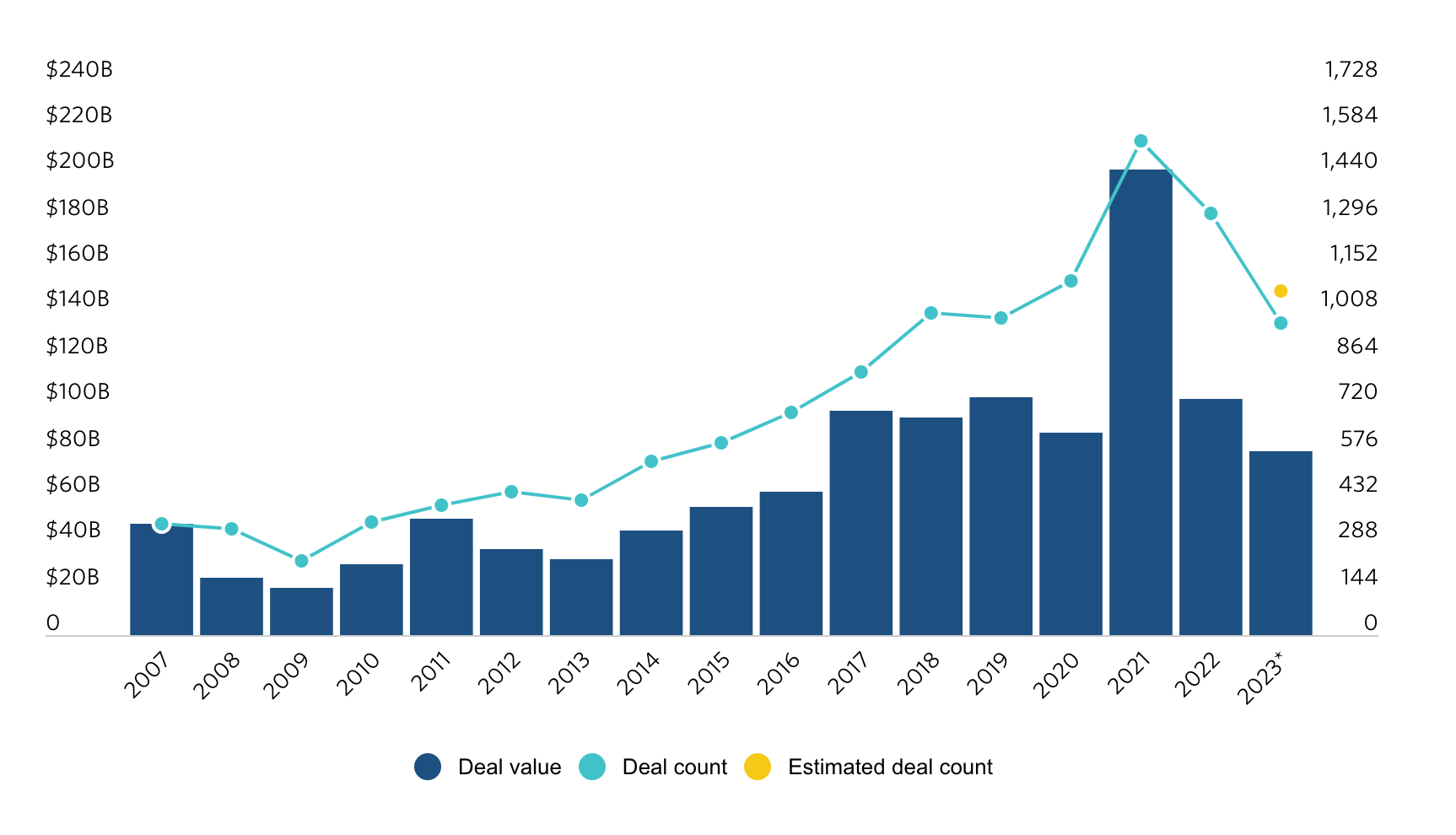

The number of PE healthcare deals has skyrocketed from just 450 deals in 2012, to over 1,300 deals in 2022! Even considering the anomaly of near-zero interest rates during the 2021-2022 peak, this deal growth has been unprecedented & relatively steady over time.

Now let’s look at some good and bad examples of PE healthcare involvement.

The Good:

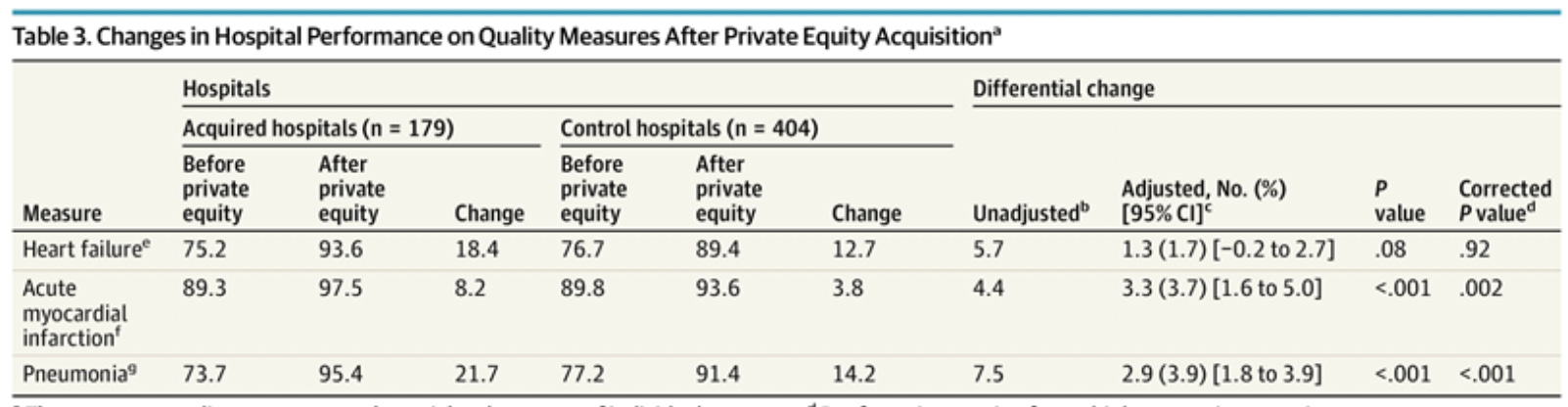

One study, published in JAMA Internal Medicine, found that after a PE takeover, hospitals actually improved on both quality measures and financial performance.

In an adjusted analysis, PE-acquired hospitals increased scores by 3.3 percentage points and 2.9 percentage points, for acute myocardial infarction (Ami2) and pneumonia (Pn2, Pn3, Pn5, Pn6), respectively.

In terms of financial performance, acquired hospitals saw:

a mean increase of $2.3M in annual net income, and

a decrease in cost per adjusted discharge of $432

Overall, the authors acknowledge that PE-acquired hospitals showed measurable improvement, yet the study is far from perfect (for example—improvements in hospital processes could reflect better patient care, but they could also just reflect a renewed focus on compliance standards/pay-for-performance contracts).

One interesting note — The share of Medicare-based discharges declined by ~1% for hospitals after acquisition. Could this be the PE firms seeking more profitable, private insurance plan reimbursements, since Medicare reimburses well below the cost of care?

I’m curious about whether PE-acquired hospitals could actively phase out Medicare plan acceptance in favor of private plans (or maybe this is common among other hospitals too?).

The Bad:

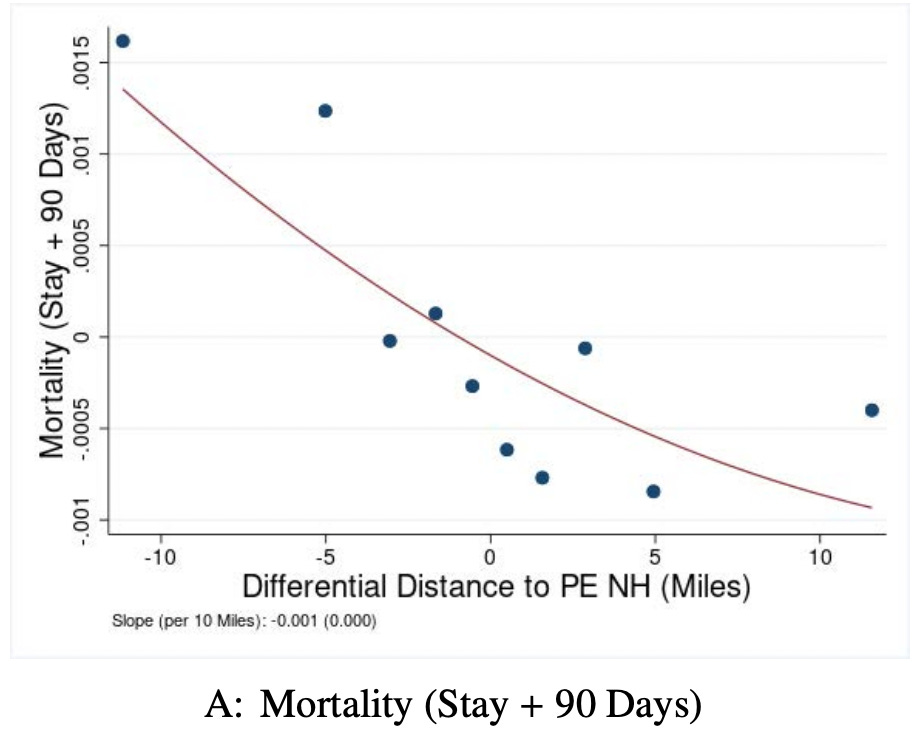

One NBER study from 2021 found that, compared to non-PE-owned nursing homes, PE-owned nursing homes had:

Increased probability of patient death by 11% (local average treatment effect)

Increased amount billed per stay per patient by 8%

Declines in patient well-being, nurse staffing, & care standard compliance

Many studies also focus on the rise in patient care costs following a PE acquisition.

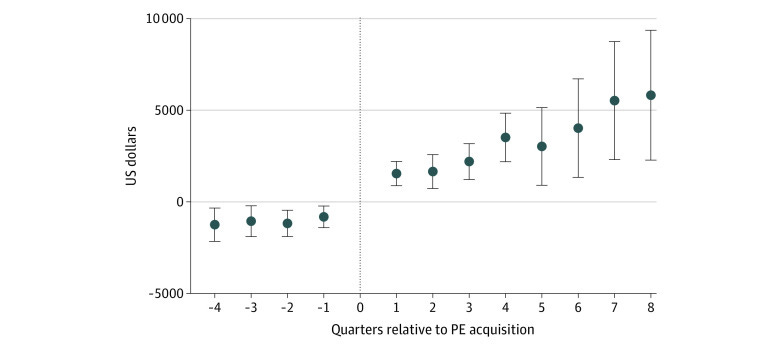

One article in the Journal of Health Economics found that in ambulatory surgery centers (ASCs), healthcare delivery was largely unchanged post-acquisition, yet charges for services did increase over time.

Specifically: after 4-5 years of PE ownership, the ASCs’ average charge per case was 50% above their baseline.

Meanwhile, the number of procedures performed per case declined by 13%. This means that post-acquisition ASCs were charging more money for less work (with little evidence that procedures got any more complex/expensive).

Another study in JAMA Health Forum found that, compared to the control physician groups, PE-owned physician groups (post-acquisition) had:

An average increase of $71 charged per claim

A 25.8% increase in number of unique patients

A 9.4% increase in share of office visits for established patients that were billed as longer than 30 mins

No change to patient risk scores

In other words, the main effect of PE acquisition was higher charges and higher utilization (e.g., of established patients), with little effect on actual care.

The Caveats:

Yes, I was only able to find one (1) study that demonstrated largely positive outcomes for a PE healthcare acquisition. But I strongly believe there should be other positive examples

Health Economics, as a field, should not be 100% trusted (much of the existing literature has nebulous value)

None of the studies mentioned have perfect measures of quality or financial performance

Most studies only accounted for three to four measures of care quality

Hospital financial performance is HIGHLY multi-faceted

For example — if a hospital “performs better” with a higher charge-to-cost ratio, this could mean a lot of things. Perhaps the hospital engaged in some form of upcoding, or they began charging more for the same services, or they simply cut operational costs. It’s hard to understand the full picture with any one measure

Failed Deals & Political Action

There’s been no shortage of PE healthcare deals ending in disaster. To name a few:

Cerberus Capital Management acquired Steward Health in 2010, and sold it in 2020. But Steward is now in deep trouble, arguably due to liabilities assumed while Cerberus was the owner (i.e., expansion at all costs led to insurmountable debts). Steward has stopped paying vendors and owes $50M in back-rent to their property owners

Prospect/Delaware County Memorial Hospital

Prospect Medical Holdings bought a cash-strapped hospital, promising to turn it around and gain long-term profitability. Seven years later, Prospect is getting sued and the hospital is closed

Leonard Green tried to leave Prospect with $1.3B in financial and lease obligations

These have all spurred action from US politicians. One example is Markey’s Health Over Wealth Act, proposed in response to the Cerberus/Steward Health situation.

A couple other recent examples:

Considering the draconian level of government involvement in proposals like the Health Over Wealth Act, it’s fair to say that PE regulation has been more aspirational than legislative. But it’s also clear that politicians are beginning to prioritize the issue.

What’s Next?

The portion of PE deals that are healthcare-based has declined steadily, from 14% in 2020 to 11% in 2023

Even as PE deals cool down from their 2021 highs, we can expect further government probing into PE healthcare ownership. Recent attempts at bipartisan investigation are just the beginning

Expect more PE deals to end badly, as PE firms find they’re unable to make hospitals profitable and/or sell to large health systems (see the Prospect/Delaware County situation mentioned above)

PE healthcare activity will likely grow outside of traditional hospital acquisitions. I’ll be following PE investments in pharma and biotech (namely, obesity treatment, Alzheimer’s cure, protein drugs, etc)

See recent deals with Syneos Health and Paragon Healthcare for reference— both biopharma plays

If we want to slow down healthcare consolidation in the US, Professors Singh and Whaley offer some interesting (though unlikely) ideas:

Tax credits for independent physician practices (already implemented by Indiana), to make practices less desperate for cash

Boosting transparency for deals both pre- and post-acquisition (as proposed in the Health Over Wealth Act)

Medicare reform to increase payments/incentives for primary care practices (which are especially cash-strapped and vulnerable to seeking PE acquisition)

Overall, this topic is impossible to fully analyze in one article. But I personally learned a lot and I think our government’s future interactions with private investment might be dictated by healthcare. Thanks for reading!